- F&A Rate Agreement (pdf)

- F&A with State of Utah

- OSP Budget Worksheet (xls)

- Budget Calculator for Varying F&A Rates (xls)

- F&A Reduction/Waiver Form

- Research Handbook > 6.3.1.2.a Generally Acccepted Waivers

- Procedure Library > Request an F&A Waiver

- Intercollegial/Departmental Agreement on the Distribution of F&A Costs (doc)

- VPR > Facilities & Administrative Distribution and Useage

- COGR > F&A and the Cost of Research

F&A (Indirect Costs)

Effective July 1, 2024, the University F&A rates are considered provisional rates.

The rates will continue to be the same as those negotiated in the previous 2021 F&A rate agreement. These will be applied until the next negotiation is completed with the cognizant federal agency, the Department of Health and Human Services (DHHS).

The provisional rate is used in proposals and sponsor billings until future rates are negotiated and individual awards can be adjusted. OSP will provide notification when the rate negotiations are complete and a new agreement is in place.

| Project Type | On-Campus | Off-Campus |

|---|---|---|

| Research | 54% | 26% |

| Instruction | 41.5% | 26% |

| Other Sponsored Activity | 35% | 26% |

For State of Utah, use rate above for federal flow-thru or 10% for all other agencies and prime funding sources. Read about this policy |

||

For help determining project type see F&A Activity Types.

Off Campus Rate

An off-campus rate of 26% can only be used if the administrative structure of the project is relocated from the University of Utah and its affiliates for more than 120 days. Use of this rate requires pre-authorization from Compliance Accounting. Read more about the off-campus rate.

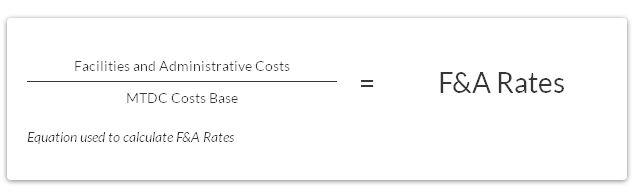

F&A Cost Calculations

F&A cost rates are based on Modified Total Direct Costs (MTDC), which is the total direct cost less:

- Equipment above $5,000

- NSF participant support costs

- Patient care costs

- Subcontract expenses in excess of $25,000 for each subcontract

- Tuition

F&A is typically applied to MTDC. This is referred to as the "F&A Base". For assistance developing a budget that spans varying F&A rates, use our budget calculator. Read more about F&A cost calculations in the Research Handbook.

Facilities and administrative (F&A) rates are the mechanisms used to reimburse the University for the infrastructure costs, i.e. F&A costs, associated with sponsored research and other sponsored agreements. F&A rates are essentially overhead rates, calculated as a percentage of the direct costs of sponsored projects. These are actual costs to the University and directly support sponsored projects being performed by the University of Utah. Sometimes F&A rates are referred to as indirect cost rates.

Read more on F&A in the Research Handbook. See also the VPRs F&A Distribution and Useage.

If a project's investigators are employed across college or departmental lines, companion projects or a statement of the intended distribution of F&A costs may be necessary for each sponsored project at the time a proposal is submitted. The Intercollegial/Departmental Agreement on the Distribution of F&A Costs (doc) should be used to detail the intention to split F&A only in lieu of establishing companion projects at time of award. The form should be uploaded into the Document Summary Sheet (DSS) in eProposal.

The University does not waive indirect costs on undergraduate student salaries. Instead, the University provides a financial incentive to encourage meaningful undergraduate participation on sponsored research projects. The University - at time of award setup - will calculate F&A collected for undergraduate salaries and put these funds toward the direct costs of the project or post-award Grants & Contracts Accounting (GCA) will automatically return overhead on any undergraduate salaries expended on research projects. This is a pre-approved institutional waiver that requires no additional authorization. Read more on waivers in the Research Handbook

The proposal budget submitted to the sponsor should include all applicable F&A. The University does not waive overhead on undergraduate salaries, we collect it and return it (on the back end) to the PI in support of the project. The budget sent to OSP to set up the project should also include all applicable F&A.

This practice used to apply only to NSF Research for Undergraduate (REU) projects but has been expanded to include any project that includes undergraduate salaries.

F&A costs are defined in OMB Circular A-21 as costs that are "incurred for common or joint objectives and therefore cannot be identified readily and specifically with a particular sponsored project, an instructional activity, or any other institutional activity." F&A costs are sometimes referred to as indirect costs. Examples of F&A costs include:

- Operating and maintenance costs such as utility costs, security costs, and custodial costs.

- Common administrative functions such as payroll and purchasing

- Sponsored project administration

Because it is impractical to account separately for such costs. F&A costs are normally not charged as direct costs to sponsored projects.

F&A rates are developed under the requirements of the U.S. Office of Management and Cost Principles for Educational Institutions. The rates are calculated according to the F&A Cost Rate Agreement for the University of Utah and negotiated with our cognizant federal audit agency, the Department of Health and Human Services (DHHS). The following rates are negotiated:

- Organized Research (On-Campus)

- Organized Research (Off-Campus)

- Instruction (On-Campus)

- Instruction (Off-Campus)

- Other Sponsored Activity, i.e. Public Service (On-Campus)

- Other Sponsored Activity, i.e. Public Service (Off-Campus)

All F&A costs within the University are assigned to cost pools related to primary functions. Then a portion from each cost pool is attributed to the research enterprise according to guidelines provided in Circular A-21. Totaling the portions of each cost pool allocated to research yields the University's total F&A costs attributable to sponsored research. The total is then converted into the F&A rate by dividing it by "Modified Total Direct Costs" (MTDC).

MTDC includes the total direct costs of a sponsored project less the cost of equipment over $5,000, capital expenditures, alternations/renovations, space rental costs, and the portion of each subaward/subcontract in excess of $25,000 within a competing segment of an award.

The actual F&A rates for most federally sponsored project awards are the standard rates referred to in the University's F&A rate agreement. While it should be customary practice to use the University's negotiated standard F&A rates on all sponsored projects, there are certain exceptions in which not all sponsors can reimburse the University for F&A costs at the negotiated rates. The following are some exceptions:

- Statutory limitations prevent some federal sponsors from reimbursing F&A costs at the federally-negotiated rates.

- Many non-federal sponsors such as state, local and private agencies have policies concerning the reimbursement of F&A costs at less than the federally-negotiated rates.

The F&A rate applied to individual awards is determined by:

- Published sponsor policy or,

- Statutory limitations or,

- The Office of Sponsored Projects (OSP) during the final negotiation of an award, generally a contract, with a given sponsoring agency.

Once an F&A rate is set with a sponsor for an individual award, it generally remains in effect throughout the entire competitive cycle of the award.

F&A costs are charged to individual awards as direct costs are incurred. The University does not recover F&A costs from sponsors until direct costs are charged to the award. F&A is typically applied to modified total direct costs (MTDC) of awards. This is referred to as the "F&A Base" and is the same base on which the University calculates and negotiates rates with DHHS. Read more on F&A cost calculations in the Research Handbook.

MTDC represents the total direct costs of a sponsored project less the cost of equipment over $5,000, capital expenditures, alterations/renovations, space rental costs, student stipends, tuition, scholarship and fellowships, participant support costs, and the portion of each subaward/subcontract in excess of $25,000 within a competing segment of an award.

| Action | Amount |

|---|---|

| A researcher buys supplies on an award | $100 |

| The actual F&A rate on the award |

51% (based on FY17) |

| The University collects the F&A cost associated with that direct cost (supplies) | $51 |

| The same researcher purchases a piece of equipment for $10,000 | No F&A cost would be collected on that particular direct cost (equipment over $5,000) |